POINT OF VIEW · 10 MIN READ

Value Creation Isn't a Budget Problem

The team you can afford still won't fit a moving portfolio.

Every year, a portfolio company has one or two things that would make the year. A data foundation that finally makes the numbers trustworthy. A risk-contracting build that changes the economics of the business. The integration that turns three deals into one platform.

They are almost never the things the team is doing. The team is keeping the business running, neck deep in the ninety other things that must be done. The one or two that would matter most sit untouched, because the fire is always today and the build can always wait until next quarter.

You run the operating team for the firm, and you watch this play out across every company you hold. So you carry some capability in-house, a standing bench on the firm's payroll, and you borrow the rest into each company when the moment comes. Every firm does both. The only real question is where the line falls between what you carry and what you borrow.

Most people draw that line with the budget. What can we afford? A firm of enough scale carries more; a smaller one borrows more. The wallet picks the model. True in theory, misleading in practice.

Budget is a real constraint, but it is a ceiling on how much capability you can field, not the rule for what to carry and what to borrow. Treat it as the rule and you have answered the wrong question: "how much value creation can we afford?" which assumes value creation is one thing to buy. It isn't. It is a mix of work of different kinds.

Hand a firm unlimited money and the line barely moves. You still would not carry a bench big enough to hold every skill every company might need, because a specialist sitting idle until the moment comes is worth less than one you borrow at the moment it's needed.

Twice, eight years apart, McKinsey has found the same thing: bench size barely tracks firm size, and the firms that can most afford a deep bench are not the ones that carry one. The wallet never drew the line. The work does.

Why you can't staff for it in advance

A permanent operating team is a single fixed bet: a set headcount, skill mix, and depth, built to a snapshot of what the portfolio needs. The portfolio is not a snapshot. The one or two builds that matter vary along several axes at once, and none stay put.

They vary by stage. A company you closed last quarter needs its operating system stood up: reliable KPIs, a planning cadence, board reporting that tells a credible story. A company three years in needs its growth made predictable, with market prioritization and a real pipeline in place of inherited contracts and gut calls. A company heading for exit needs its operations cleaned and its numbers ready to defend. Every company walks that arc, the portfolio holds all of it at once, and the mix shifts every quarter as new deals close and exits finalize.

They vary by business model. A multi-site services roll-up runs on labor, throughput, and payer mix. A patient-engagement software platform runs on product, retention, and R&D. No standing bench holds deep specialists in both: a generalist is too shallow on each, and a specialist cannot span the set. The expertise a given company needs is rarely the expertise you staffed.

They vary by thesis. One company's plan is a cost takeout, the next is a roll-up, the next is organic commercial growth. Each calls for a different build, and your portfolio is running all of them at once.

And they vary by where each business is broken: finance at one company, the commercial engine at the next, revenue cycle at a third. The team's functional composition is fixed, and the constraints are scattered and moving.

No bench covers that. Hire for today's portfolio and you are mis-staffed by the time the next two deals close. You cannot recruit your way out. A fixed team will always trail a moving portfolio.

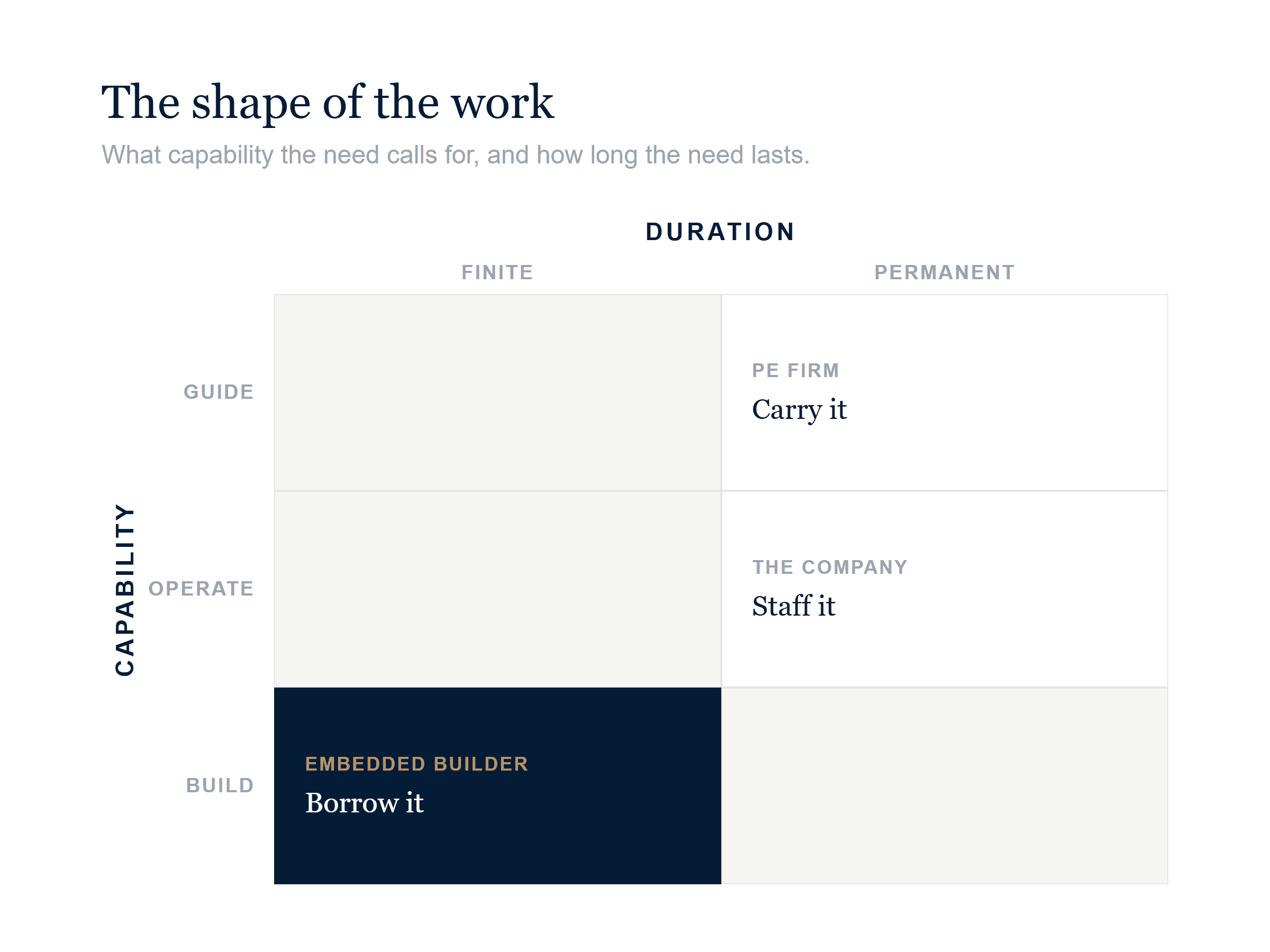

The shape of the work

So you sort the work, you do not staff for it. Two features sort it: what capability the need calls for, and how long the need lasts.

Capability comes in three forms. Guide is the operating partner's work: the diagnosis, the benchmark, the read on what good looks like at this stage. Operate is running a seat that already exists: a CFO's chair, a function that has to keep working. Build is standing up what was not there before: the operating cadence the business runs on and the board requires.

Duration has two settings. Finite: the work has a defined end, and when it is done the need is gone. Permanent: it recurs for as long as you own the company.

Where the work lives

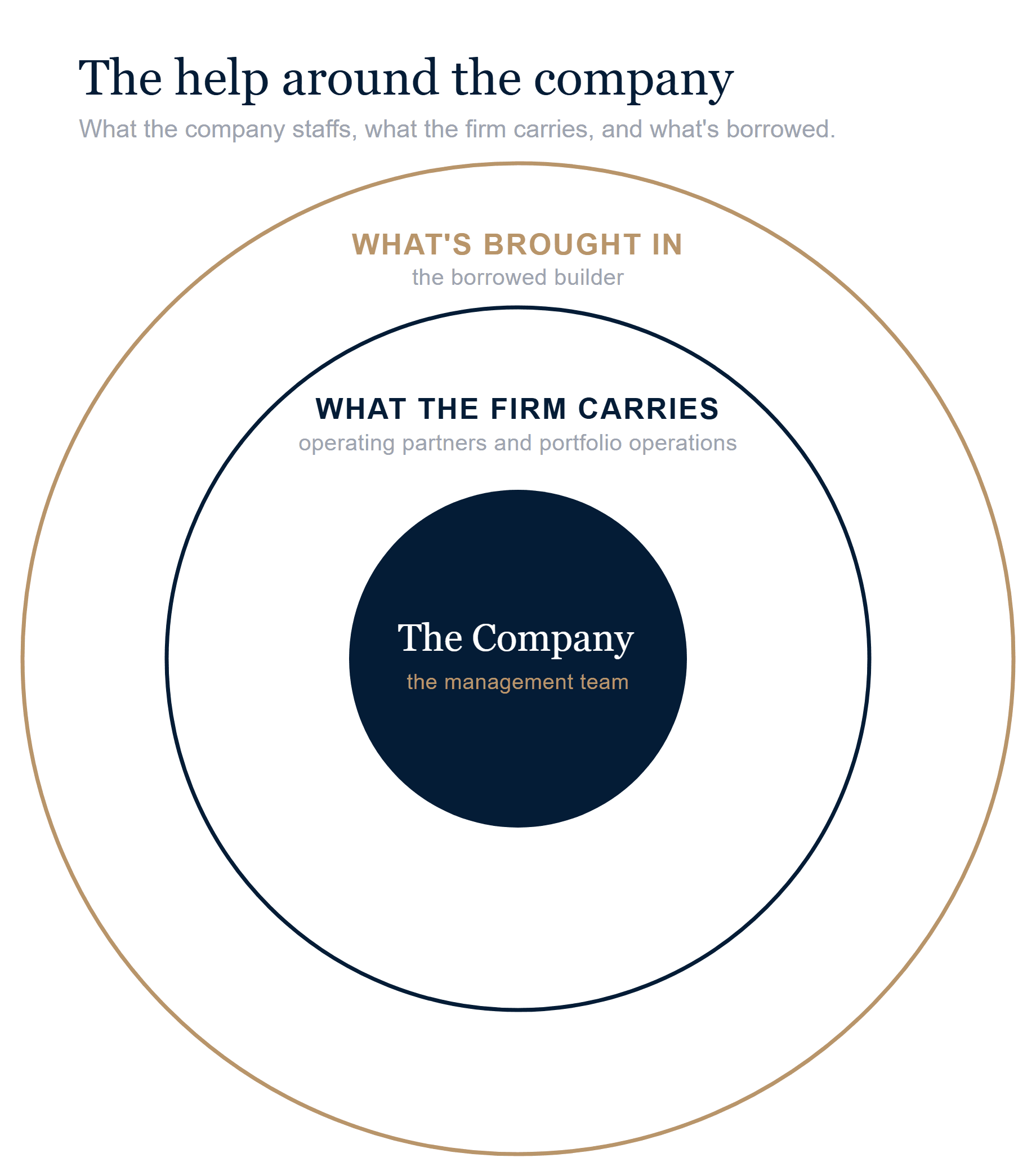

Cross the two and each kind of work has a place. Three answers, arranged around the company in layers.

The company staffs the day-to-day. The center, on its own payroll, running the business. The most important seat there is.

The firm carries a standing bench. Lean, on its own books: operating partners who guide (the diagnosis and the benchmark) and portfolio operations who orchestrate (sensing where a company strains, deciding which build is worth doing, routing the help in). Neither one builds.

The rest is borrowed from outside. The embedded builder for the build, the finite thing the company has never done before, and preferred vendors on call for the specialized work that recurs at every company.

The sponsors who have been at this longest draw it the same way, as rings around the company. The build comes from the outer ring. The center is busy running the business. The build spans every function and has no natural owner, so it falls to leaders who are already full. The work gets done in the margins, at half attention, or not at all.

Portfolio operations is what closes the gap. It senses the strain and routes the builder in, and the builder stands the thing up from inside, hands it to the team, and goes.

Borrow the build

Of the three, the build is the one that decides the year. It is the one or two things a company does for the first time, and the work the day-to-day will always starve. Build the data foundation once, switch the EMR once, stand up risk-contracting once. Left to the team running the company, it waits forever, because the fire is always today.

Take the move every growing company eventually makes, from QuickBooks to NetSuite. Buying the system is the easy part, and there is a vendor for exactly that, a NetSuite partner who runs the same implementation at every company and hands back a configured system. But a configured system is not yet a finance function.

The build is the chart of accounts redrawn, the close re-sequenced, the reporting the board will actually read, and the team running on all of it by quarter-end. That work spans every function and belongs to none, so left to the people closing the books each month, it slips. The platform goes live and the real numbers stay in spreadsheets. The vendor installed the software. No one built the capability.

The answer is to over-resource it. No one ever regretted putting too much weight behind the one or two things that would make the year. The company could grind it out on its own, slowly, while its people keep the lights on. Better to bring in someone who has built it before, focused on the one or two that matter, and let them build while the company runs.

The hard part was never deciding what to build; it is building it while the business runs. A borrowed operator who has done it lands on the answer and leaves when it is done. A senior operating partner at one of the largest firms put it plainly: bring in a specialist who has done it time and again, let them do it, then let them move on.

And it has to be borrowed into the company, not built on a bench back at the firm. Work defaults to wherever the builder sits. Build it from the firm and you get oversight, reporting, and direction, and all of it deteriorates when attention rotates to the next deal. Build it from inside the company and the company owns what gets built. It has to be built in place, where it will be run.

Where borrowing goes wrong

Four roles get mistaken for the build. From the outside, each shares its silhouette. The work underneath does not.

A strategy consultant runs a one-off analysis: the org review, the RCM assessment. It diagnoses and recommends, then leaves. The build falls back on a team already at capacity.

An interim executive keeps an existing seat running through a gap. It fills a people-shaped hole, not a capability-shaped hole, and builds nothing new.

A full-time hire earns its seat only where the work never ends, like perpetual M&A. Pointed at a finite build, it outlives the work and manufactures more to justify the hire.

The fourth is the one you already have. An operating partner gives ongoing guidance and the read on what good looks like. It names how the business should run and leaves the running to someone else. It guides, never builds.

That is the most expensive confusion, because the operating partner is already on the payroll, so reaching for it feels free. But the operating partner answers to the board and has done the job before. So when one steps in to build, the CEO sees a successor learning the business and stops sharing what the build depends on. And the role tends to draw late-career advisors, the ones past wanting to do the work themselves. The business gets its gap named, and the build still waits.

The embedded builder is the one you borrow, the only role meant for the one or two builds: an operator who has done it before, badged into the company, who stands it up from inside, hands it to the team, and leaves it owned by the company. The others look like the build. This one is the build.

The objections, and the answers

Borrowing the build draws two honest objections, and they pull in opposite directions. Either the borrowed help never leaves, or everything it knows leaves with it.

The first objection is earned. The consulting business model is a pyramid: partners sell the work, associates bill it, and the margin lives in how many associates each partner keeps deployed. Every sponsor has read the four-phase proposal where phase one was the entire project and the other three phases existed to keep the meter running.

The same model is why a $30 million company gets a proposal staffed with a partner and three associates. A company that size cannot absorb it. Four outsiders in every meeting, on a management team of six, and the work of managing the help crowds out the work.

The early phases are priced to land. The later phases are sold into the dependency the early work created. The engagement has to grow for the model to work.

There is a different way to borrow. One operator who has done the work before, badged into the company, with their own name on the build. No pyramid underneath them, no meter to keep running.

Put that shape of borrowing inside a portfolio and the incentive flips. The company writes the check. The next call comes from the firm, and the firm owns the next company, and the one after that.

A clean finish at one company wins the next deployment. Dragging a build out forfeits the rotation. The sponsors who borrow best run it exactly that way: in, build, out, on to the next company they own. No contract enforces that discipline. Wanting the next deployment does.

The second objection is just as fair: the knowledge leaves when the project ends. The usual answer treats borrowed help as the cheaper option and accepts that it eventually walks out the door.

That is a design failure, not a property of borrowing. A build survives when the handoff is engineered from the first week instead of bolted on at the end, with named internal owners and systems the team holds and edits.

I ran one of these at a payer-backed MSO platform in the Northeast. The engagement was a finite build of the business development infrastructure, the pitch, and the lead-generation, designed from a blank page and handed to the company's own team. They ran it without me and took provider enrollment from 97 to 170 in under a year. The build was borrowed. What it built stayed.

The builder leaves. The build stays. That is the whole point.

What this decides

Sort the work and you know where each kind lives: what the firm carries, what the company staffs, and the build borrowed from outside.

That alone stops the most expensive mistake: staffing a fixed team against a portfolio that will not stand still. Keep your core lean, shaped to the work that recurs no matter what the portfolio does. Let each company run what it owns.

Most firms have already built half of this. They keep a short list of preferred vendors for the specialized work, pre-vetted and pre-negotiated, the same names offered to every company they own.

There is no equivalent for the build. The operator who can stand up the one or two things that would make the year is still found from scratch, at every company, every time. You have curated a vendor list, not a build bench.

That is the gap to close. For the one or two that would make the year, borrow them, build them, and leave them to live in the company.

McKinsey, "Private equity operating groups and the pursuit of 'portfolio alpha'" (2018); and Global Private Markets Report, private equity chapter (2026).

MARTEL CAMPBELL

Replies welcome: martel@martelhealth.com

© 2026 Martel Health